What is The Depository Trust and Clearing Corporation (DTCC)?

DTCC is a financial market utility (FMU) that was established more than 45 years ago to provide clearing and settlement services for the financial markets. While the investing public is very familiar with the front end of trading, such as brokers and the exchanges, FMUs are the organizations, systems and networks that provide the underlying infrastructure to enable the financial markets to operate seamlessly. They can include payment and settlement systems, clearinghouses, and depositories.

What is DTCC’s role in the financial markets?

In the U.S., DTCC operates three clearing agencies:

- National Securities Clearing Corporation (NSCC)

- Fixed Income Clearing Corporation (FICC)

- The Depository Trust Company (DTC)

These subsidiaries deliver highly efficient clearing services across the U.S. equities and fixed income markets, reducing risk and cost for financial firms and, ultimately, the end investor, while ensuring safety and reliability in the marketplace. DTC provides clearing and settlement services for virtually all equity, corporate and municipal debt trades and Money Market Instruments in the U.S.

Because DTCC plays a critical role in the financial markets, who regulates these businesses?

We are regulated by more than 20 different supervisory bodies globally. In the U.S. alone, different parts of our core business are regulated by the Federal Reserve, the U.S. Securities and Exchange Commission and the NYS Department of Financial Services. Our three clearing agencies are also designated as Systemically-Important Financial Market Utilities (SIFMUs) under Title VIII of the US Dodd-Frank Act.

What exactly does it mean to be designated a SIFMU?

Dodd-Frank created the U.S. Financial Stability Oversight Council (FSOC) within the U.S. Treasury Department with a mandate to monitor the stability of the financial system. The SIFMU designation is a recognition of the criticality of these services to the smooth functioning of US financial markets. As a result, we are required to meet strictly prescribed risk management standards and face heightened oversight by U.S. regulatory authorities. These rules were implemented to protect the global economy and the investing public from a financial crisis similar to, or worse than, what the world experienced in 2008.

You mentioned earlier that DTCC provides clearing and settlement services. What exactly does that mean?

When an investor buys or sells shares in a stock, that transaction is routed to a clearinghouse. After a trade is compared and verified, the clearinghouse steps in between the two sides, and regardless of what happens to either party, it guarantees the trade will be completed. This provides certainty for investors and improves market safety by lowering exposure to settlement failure.

Our most important responsibility is guaranteeing trade completion in the event that one or both parties to that transaction defaults.

Can you share an example of when this happened?

If you think back to the financial crisis of 2008 and the bankruptcy of Lehman Brothers, which was the fourth largest investment bank in the U.S. at the time, we made sure those trade were completed and that every buyer received their securities and every seller got their money.

In the weeks that followed the Lehman bankruptcy, DTCC successfully closed out more than $500bn in market participants' exposure from the bank's collapse, the largest close-out DTCC has ever managed. The liquidation of Lehman was complex, involved multiple asset classes and required a methodical approach to mitigate potential losses from outstanding trading obligations. If you were a client of Lehman or traded with them at the time of their default, you didn’t need to worry about receiving your securities or money because DTCC had guaranteed your trade.

How is DTCC able to do this when there are, on average, more than 100 million broker-to-broker transactions per day with a value of nearly $1.2 trillion?

Many in the financial industry know that DTCC’s role is to provide stability during times of crises.

After 9/11, for example, DTCC was able to steady a shaken financial system by clearing and settling trillions of dollars of trades. But this stability and risk mitigation is what we provide to firms and the industry every day. Banks, brokerages and other members of our clearinghouse deposit margin with us to protect against the risk that a member defaults on its obligations to settle its transactions. This might be cash, U.S. treasuries and other highly liquid assets. Margin is the core risk management tool that protects against the risk of a member default.

How exactly does the margin process work?

Every day, our clearing members are required to post margin with us. Margin amounts, which are unique to each member firm and risk profile, make up what we call our Clearing Fund. Margin is collected at the start of each day and in some cases can be collected intraday if there is a lot of market volatility. The margin we collect is primarily based on established calculations that are subject to our rules, and we provide reporting and other tools to our clearing members to help them anticipate their margin requirements for a particular portfolio. NSCC’s margin requirements are developed with stakeholder feedback, which includes clearing member engagement, and require regulatory engagement and approval.

Margin plays a critical role during these times because extreme volatility can generate substantial risk exposures at firms that clear trades with us. As the risk of a clearing member’s portfolio increases, the amount of margin collected also increases, in a calculation called “VaR,” or Value-at-Risk. This margin capacity allows us to protect investors by efficiently and safely winding down positions in the event of a member default without the industry or investors suffering losses. This mitigates risk for the global financial marketplace by ensuring that a single firm’s default does not spread into a market-wide contagion.

During times of market shocks, does DTCC tell banks or brokerages they can’t trade certain securities?

No, DTCC does not impose restrictions on clearing members as to what securities they may trade or what types of trades they may accept. Clearing members that are concerned about the margin requirements they will face may choose to impose risk controls or other trading restrictions on their clients to limit the risk in their clearing portfolios and the margin requirements they are likely to have at the clearinghouse.

Learn more about how market infrastructures like DTCC are leading change to protect and shape the future of capital markets.

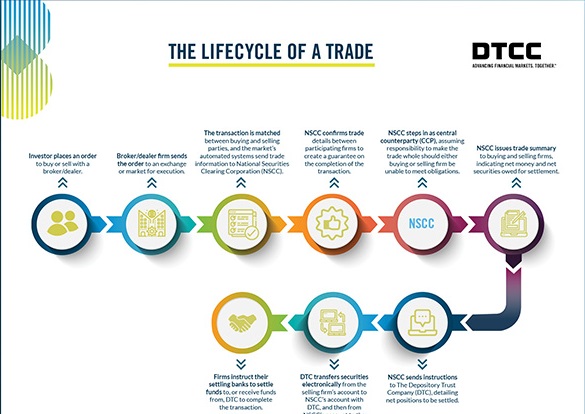

Please click on this image to download an infographic on the lifecycle of a trade